A solid outcome to round out 2022

NAB Group Economics

Overview

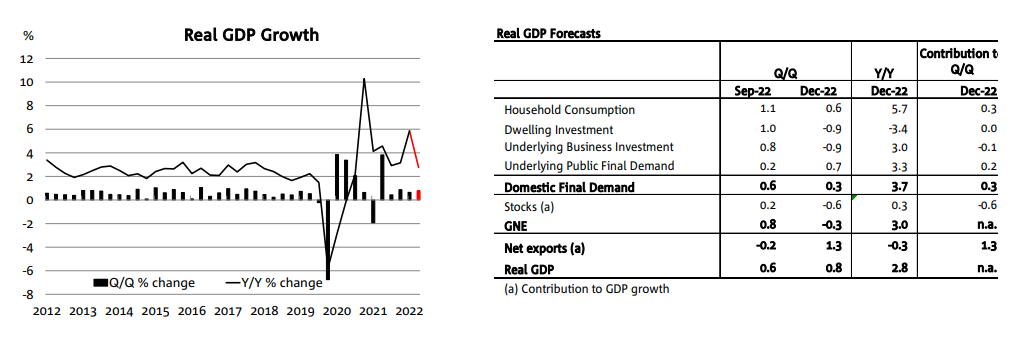

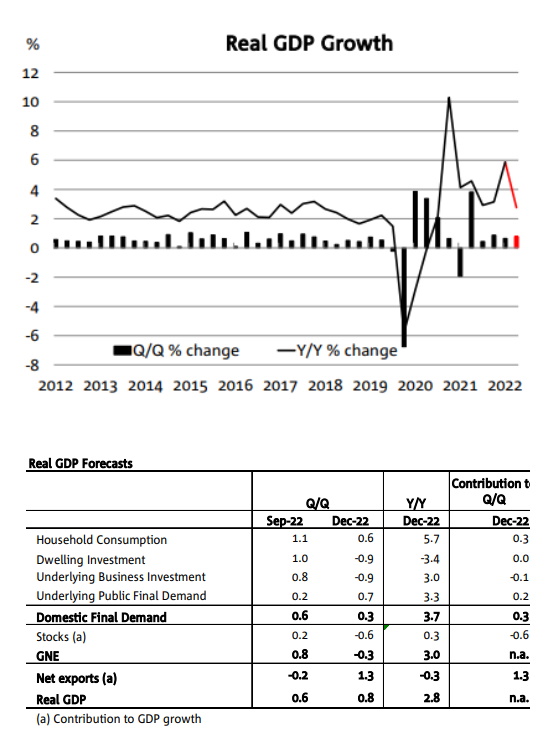

NAB sees a 0.8% q/q (2.8% y/y) GDP print for Q4 2022. Household spending looks to have remained resilient to rising rates and inflation. In part, this reflects the ongoing recovery in services spending. Elsewhere, investment looks to have fallen slightly, while net exports will provide a large boost, partially offset by the stock cycle. We expect the production and income sides of the accounts to reflect the broader trends unfolding in the economy, with services industries seeing gains, while goods industries generally remain resilient. Labour cost measures will see strong prints reflecting the ongoing tightness in the labour market. This release will be unlikely to shift the dial for policy with the RBA squarely focused on managing the risk of broadening inflationary pressure amidst the strength in domestic demand. Indeed, these accounts will show that the economy has remained more resilient than expected

- GDP is expected to have risen by 0.8% in Q3 (2.8% y/y). Retail sales declined by 0.2% in Q4, though our internal transactions data suggests that services spending offset the softness, with overall consumption up around 0.6%. Partials for dwelling investment point to a small gain in new building but a large pull-back in renovations. Business investment looks to have fallen at face value with a weak outcome for non-res building and engineering construction. However, the capex numbers for buildings & structures suggest a stronger outcome. While the work done numbers typically map through to the national accounts measure of investment the Capex survey may be more reflective of trends at the smaller end of the scale which are not captured in the building activity survey.

- The price and wage measures of the accounts will again garner more focus than usual. Average earnings per hour will provide a clearer signal on labour cost pressures than the narrow WPI print earlier this week, while the nominal unit labour costs measure will also provide some insight into the inflationary pressure from wages growth in a tight labour market. The domestic demand and consumption deflators, which have reflected the broad-based strength in prices recent quarters, are expected to remain high. The terms of trade will also likely see some volatility due to movements in commodity prices but remain high – and is important for assessing the broader income boost at play in the economy in addition to the strength in employment and wage growth.

- The stocks and trade contributions are key sources of uncertainty. Stocks have been volatile over recent quarters as supply chain impacts have driven strong cycles in inventories while there was also a large run up in mining inventories in Q3 which could well be unwound. That said, there is also likely some offsetting support from the ongoing rebuild in inventories which were run down amidst strong demand through the pandemic. Similarly, large movements in key commodity prices leads to greater uncertainty on real trade volumes estimated from the nominal monthly trade data.

- Looking forward, we expect growth to slow sharply from here, driven by flat to negative outcomes for consumption in H2 2023 as the full impact of higher rates and inflation flows through. Goods spending is expected to moderate, though there may be some ongoing recovery in services spending. Dwelling investment and business investment are expected to weaken, though we expect a small positive offset from net exports. With ongoing volatility in the trade numbers, a focus on domestic demand will be important for policy – particularly for consumption but as the volatility fades there, trends in the smaller components of GDP will become more important for overall growth. The magnitude of the expected decline in dwelling investment, the direction of business investment amidst greater uncertainty but still-high capacity utilisation, and the strength of government spending will all be important swing factors.

- This release is unlikely to impact the path of monetary policy in the near term with the RBA having already signalled further increases in coming months. Indeed, the national accounts prices and wages measures will likely confirm the broad-based inflationary pressure in the economy. Labour costs measures will likely provide more evidence of the pressures on wages than this week’s WPI print. Ultimately, the RBA has signalled that there will be further increases in coming months based on a forward looking reaction function and their latest set of forecasts. That said, slowing growth will likely be the first signal the economy is cooling in response to rate rises alongside the moderation in global inflation. Therefore, activity partials – particularly for consumer spending – will be important in assessing the flow through in policy over coming months. NAB continues to see the RBA hiking rates by 25bps in March, April and May, taking the RBA cash rate to 4.10%.

Group Economics

Alan Oster

Group Chief Economist

+(61 0) 414 444 652

Jacqui Brand

Executive Assistant

+(61 0) 477 716 540

Dean Pearson

Head of Behavioural &

Industry Economics

+(61 0) 457 517 342

Australian Economics and Commodities

Gareth Spence

Senior Economist

+(61 0) 436 606 175

Brody Viney

Senior Economist

+(61 0) 452 673 400

Phin Ziebell

Senior Economist

+(61 0) 475 940 662

Behavioural & Industry Economics

Robert De Iure

Senior Economist –

Behavioural & Industry

Economics

+(61 0) 477 723 769

Brien McDonald

Senior Economist –

Behavioural & Industry

Economics

+(61 0) 455 052 520

Steven Wu

Senior Economist –

Behavioural & Industry

Economics

+(61 0) 472 808 952

International Economics

Tony Kelly

Senior Economist

+(61 0) 477 746 237

Gerard Burg

Senior Economist –

International

+(61 0) 477 723 768

Global Markets Research

Ivan Colhoun

Chief Economist

Corporate & Institutional

Banking

+(61 2) 9293 7168

Skye Masters

Head of Markets Strategy

Markets, Corporate &

Institutional Banking

+(61 2) 9295 1196

Important notice

This document has been prepared by National Australia Bank Limited ABN 12 004 044 937 AFSL 230686 (“NAB”). Any advice contained in this document has been prepared without taking into account your objectives, financial situation or needs. Before acting on any advice in this document, NAB recommends that you consider whether the advice is appropriate for your circumstances.

NAB recommends that you obtain and consider the relevant Product Disclosure Statement or other disclosure document, before making any decision about a product including whether to acquire or to continue to hold it.

Please click here to view our disclaimer and terms of use.